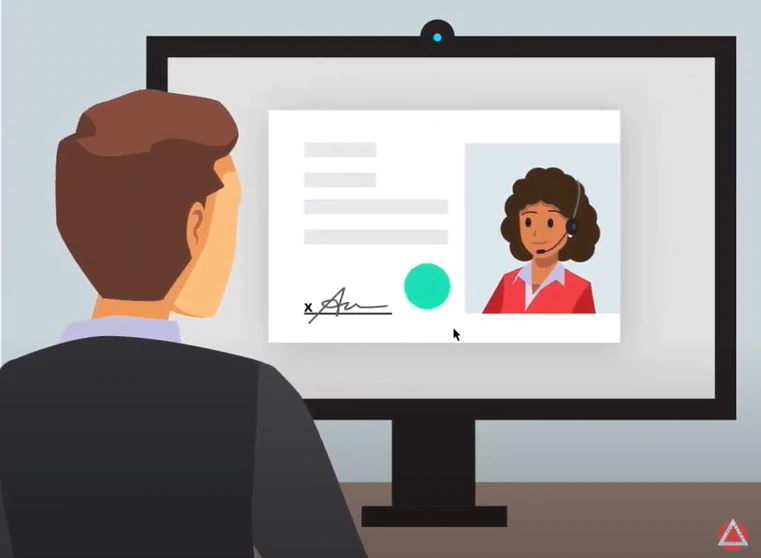

The basic steps of a remote online notarization are equivalent to a paper-based, in-person action, but the tools used are all digital. (Courtesy of the National Notary Association)

By Harvey S. Jacobs

June 22, 2020 at 9:00 a.m. EDT

On July 25, 2000, the first paperless real estate transaction took place in Broward County in Florida. That transaction involved a home purchase and financing and took less than five minutes to record. Immediately, recorded documents were returned to the settlement agent via email and images of the documents were available on the county’s website.

Two decades later and despite the threat of the novel coronavirus pandemic, many real estate transactions are still being conducted the old-fashioned, high-contact way. Home buyers, sellers and real estate agents meet at the settlement attorney’s office at the same time, provide government-issued photo identification and sign legally binding documents under oath before a notary public. The notary then signs those documents and affixes a seal on dozens of separate legal documents. The live notarization requirement has, until recently, prevented end-to-end digital transactions, but that rule is rapidly evolving.

The coronavirus has forced county recording clerks, mortgage lenders and the title insurance industry to expedite rules to permit remote online notarization (RON) closings under strict guidelines. RON closings no longer require the signer and the notary to be in the same room — they could be anywhere on the planet. Home buyers, sellers, lenders, real estate agents and settlement attorneys no longer need to gather in the same room. Buyers and sellers can take more time to review and sign settlement documents. Another benefit is that the actual closing document signing is recorded using encrypted, tamper-evident, audio and video technology. This record will then be stored and retrievable in electronic format for at least seven years.

As of mid-June, 26 states allow RON closings, including Virginia. The District and Maryland allow RON closings on a temporary, emergency basis. According to Diane Tomb, chief executive of the American Land Title Association (ALTA), nearly 30 percent of title and settlement companies are offering some type of digital closing to meet social distancing requirements. This is up from 17 percent of companies offering digital closings in 2019.

In March, the Senate and House introduced bills to authorize all U.S. notaries to perform RON. The bills would require that RON notaries use tamper-evident technologies, prevent fraud by using multifactor authentication for identity proofing, and make and retain audiovisual recordings of the transaction. It would allow signers outside the United States, such as military personnel, to securely notarize documents. It would also permit states to customize their own statutes and to recognize RON between states. The National Association of Realtors, the Mortgage Bankers Association and ALTA all support the bills. “Protecting consumers remains the title insurance industry’s top priority,” Tomb said.

Despite this regulatory groundswell, unless all parties agree, closings cannot be conducted using RON. To help lenders make decisions about allowing RON, the Mortgage Industry Standards Maintenance Organization created standards to certify technology providers that use consistent and best practices to secure confidential data. “Expanding the availability of RON is a priority” for the standards organization, said its president, Mike Fratantoni.

The National Notary Association identifies seven technology providers who are servicing the burgeoning RON industry. RON laws require tamper-evident technology, meaning that the settlement is recorded by an encrypted audiovisual record, where the notary and the signers can see, hear and communicate with each other in real time.

A notary’s main role is to identify the signers. With RON, signers must correctly answer computer-based questions about their life, credit or financial history. Signers scan credentials, and the technology provider analyzes if a credential is counterfeit, altered or expired. The notary must view the signer’s credential on camera and compare the information and image on that credential to the signer’s visual appearance, just as a face-to-face notary would examine a signer’s physical driver’s license.

Fannie Mae and Freddie Mac, which buy more than 40 percent of residential mortgage loans, have modified their single-family seller guidelines to permit RON closings in 43 states. Freddie Mac has specific temporary regulations regarding RON for closing documents, powers of attorney and electronic promissory notes.

Harvey S. Jacobs is a real estate lawyer with Jacobs & Associates Attorneys at Law LLC in Washington. He is an active real estate attorney, investor, landlord, lender and settlement attorney. This column is not legal advice and should not be acted upon without obtaining your own legal counsel. Contact him at jacobs@jacobs-associates.com, www.jacobs-associates.com, ask@thehouselawyer.com, or call 301-417-4144.

Make sure your agreement with a property manager explicitly states how repairs and maintenance are handled and how they are paid. (iStock)

Published on May 27, 2020 at 9:00 a.m. EDT

Q: Over the years we have acquired a small residential rental portfolio that we self-manage. Despite the current market uncertainty, we believe the market for rentals will be strong for the foreseeable future. We want to expand our portfolio and believe hiring a property manager will allow us to focus on that goal. How do we go about locating and selecting the best property manager? What legal terms should be in the property management agreement?

A: To find the best property manager for your situation, narrow your candidates by taking the following steps:

Make sure your candidate is properly licensed

The District of Columbia Real Estate Commission’s website provides a tool to look up licensed property managers. To obtain a property manager license in the District of Columbia, the candidate must be able to read, write and understand English; pass the commission’s exam; be a high school graduate or equivalent; not have been denied a license in the past year, and not have had a previous license suspended or revoked in the past three years. Having a real estate broker’s license is not essential, but any licensed real estate broker in the District also meets the requirements for licensure as a property manager.

Investigate your candidate’s experience, reputation and professional credentials

“You will want to select a property manager that has been in business for many years [and] enjoys a reputation for honesty, competence and technical savvy,” said Steven Landsman, president of Abaris Realty in Potomac, Md., a property management firm representing 150 condominium and homeowner associations. Call references from your candidate’s current and previous clients. Ask how long they used the candidate, if they experienced any problems and how the candidate resolved those problems. Ask the candidate how many properties they have under management and how many employees they have serving those clients.

Steven Moretti, who owns Moretti Management Group in Potomac, Md., said investors should watch out for companies that try to solicit more new business than they can reliably manage. “The problem with building a large account base without having a solid infrastructure in place is they don’t deal with all the issues that arise in a timely manner. Failure to immediately follow up on repairs adversely impacts the property and damages the tenant-owner relationship.”

Professional managers will often possess professional certifications, such as the Certified Property Manager designation awarded by the Institute of Real Estate Management, and will have joined relevant trade associations, such as the National Association of Real Property Managers.

Carefully negotiate the property management agreement

Management rates are based on the monthly rent collected and range from 5 to 10 percent. At a minimum, the agreement must clearly list the services the manager will perform without additional fees. The base fee should include collecting rent; maintaining all insurance policies; enforcing your leases in court if necessary (but not the legal fees paid to attorneys), and ensuring compliance with all homeowner association or condominium covenants, conditions, restrictions and house rules. You should also expect to pay additional fees to property managers for handling insurance claims, major repairs and capital improvement projects.

Property managers typically charge owners additional commissions for leasing vacant rental properties. These commissions typically range from a half to a full month’s rent. According to Heather Norwich, a property manager with Pier Associates in the District, “that fee covers the marketing and Internet-based advertising tasks; evaluating rental applications, running credit, criminal background and eviction checks.” A property manager’s role is to cover logistics so the owner does not need to interact with the tenant, she said. “I also handle the leasing package, make sure that the owner has the necessary District general business license and coordinate all inspections and showings.”

At some point you may decide to sell your rental unit. Pay attention to how your property management agreement treats a sales transaction. Some agreements contain clauses that obligate you to pay a commission to your property manager if you or anyone else sells your property while the property management agreement is in force and even for a period after it ends. That post-agreement period is called the “tail period.” You should avoid these embedded “exclusive rights to sell” clauses, or at a minimum, reduce the commission rate and shorten the tail to perhaps 30 days.

Many property management agreements provide the property manager with an “exclusive agency agreement,” granting them the right to sell your property for a limited time, such as 90 days, and the right to earn an agreed-upon sales commission if they sell it during that time. In either an exclusive right to sell or an exclusive agency agreement situation, you should negotiate a commission waiver or discount if you sell to your tenant, specified neighbors, friends or family members without any help from the property manager.

Still other property management agreements are silent regarding the possible sale. The implicit assumption in those cases is that since the property manager has performed well, knows your unit, and knows the sales market for your unit, you would probably call on them to list your unit for sale.

Make sure your agreement requires the property manager to provide you with all leases, modifications and renewals; tenant contact information; all keys, fobs and access control codes; and monthly and annual financial reports.

Your agreement should permit you to immediately cancel it for “cause.” Cause is often defined as a property manager’s criminal conduct, gross negligence or failure to account for and promptly disburse funds. You should also be able to cancel the agreement without cause on 60 days’ written notice.

Repairs often become contentious between owners and property managers. Make sure your agreement explicitly states how repairs and maintenance are handled and how they are paid. Most property managers’ base fee will cover handling run-of-the-mill maintenance and repairs. They outsource these tasks to contractors and should bill you for the actual cost without any markup or additional cost.

Watch out for managers that use repairs to increase their profit, Moretti said. “Many property managers maintain in-house contractors and receive extra compensation for making repairs,” he said. “Some property managers will outsource to third-party contractors and add a 5- to 15-percent administration fee to the repair cost. Still other less-ethical property managers will not charge the administration fee but will have the contractor inflate the repair cost and receive a kickback from that contractor.”

Despite taking these steps, there is no guarantee that you and your property manager will be a good fit. After all, property management is not just about managing the property condition. It is about maintaining happy tenants who pay market rent and remain in your investment properties for many years.

Harvey S. Jacobs is a real estate lawyer with Jacobs & Associates Attorneys at Law in Washington. He is an active real estate attorney, investor, landlord, lender and settlement attorney. This column is not legal advice and should not be acted upon without obtaining your own legal counsel. Contact him at jacobs@jacobs-associates.com, jacobs-associates.com or ask@thehouselawyer.com, or call 301-417-4144.

Q: We have a flip that we put on the market right before the coronavirus crisis hit. The target buyer for our house is a first-time home buyer relying on a government-backed loan, and showings have dropped to zero. We want to take it off the market until things stabilize and rent it out short-term. We want to make a rent-to-own offer to tenants, but we need to figure out the details and prepare a contract. Can you tell us how these agreements work and if they are risky?

A: These “rent-to-own” arrangements are also called lease-option agreements. They can take many forms, but basically, your tenants sign a lease containing clauses that give them the option to buy the home at a fixed price and at a fixed time, called the “exercise date.” The purchase agreement should contain all other mutually agreeable terms and conditions that you would find in a traditional purchase and sale agreement.

Typically, to induce tenants to enter into a rent-to-own agreement, you agree to apply a portion of their monthly rent as their earnest money deposit, which gets applied toward their purchase price at settlement if they exercise their option to buy. If they do not exercise their option to buy by the set date, they forfeit their accrued earnest money deposit. There are many permutations on this basic theme, depending on your and your tenant’s needs.

Usually, the rent is above fair market value, since some percentage will be applied to a tenant’s earnest money deposit. Depending on the market conditions, it could also be at or even below fair market rental value. You may wish to adjust your agreed-upon purchase price to reflect whether you believe prices will go up or down by the exercise date and to account for the fact that you are applying a portion of the rent each month toward your tenant’s eventual purchase price.

For example, you could lease your home for $2,000 per month and agree to apply $500 per month toward the earnest money deposit. After the first year, your tenants will have $6,000 saved toward the purchase price. If they exercise their option, you apply the $6,000 as their earnest money deposit toward their purchase price. Your tenant and their lender will have to come up with the remainder of the purchase price at settlement. If they decide not to buy on the exercise date, you keep the $6,000. Then they either remain as rent-paying tenants or move out and you sell to another buyer.

Rent-to-own contracts are often used in a buyer’s market when buyers, especially first-time home buyers, have a stable income, but not the cash saved for the down payment. Similarly, rent-to-own agreements can be useful when tenants’ current credit may be insufficient to qualify for a mortgage, but they anticipate their credit will improve by the exercise date and they can then qualify for a mortgage.

A variation is an “agreement for deed,” where a seller agrees to sell the home to tenants, but the deed does not get conveyed to the tenants until they pay an agreed-upon monthly amount for an agreed-upon period. The seller only conveys the deed to the property after the tenants have made the required payments. If tenants fail to make the required payments or otherwise default, they forfeit the right to the deed and all payments made up to the time the default occurred.

There are many risks associated with these transactions. For example, your tenant may damage or fail to maintain your home in a satisfactory manner. Your tenant may not leave voluntarily at the lease expiration, requiring you to resort to an expensive and time-consuming judicial eviction. There is always the risk that your tenant may not be able to qualify for a loan by the settlement time. Perhaps the biggest risk for a seller is to agree to a sales price that is below the fair market value at the exercise date. If the property appreciates more than the seller anticipates, the seller may be leaving money on the table.

The tenant also bears risks. For example, a seller may further encumber the home by taking out additional mortgages or drawing on existing home equity credit lines. If the seller does that, the purchase price may no longer be enough to allow the seller to convey the home free and clear. Other risks arise if a seller dies or becomes incapacitated. If that occurs, the home could be tied up in probate or other legal proceedings for years. An unscrupulous seller could sell the home to someone else. Such a sale would be illegal, but the tenant would then have to successfully sue the seller for damages and might not be able to void the illegal sale. One way to reduce the tenant’s risk is to record the lease in the land records of your state. By recording the lease, the public is on notice that the tenant has an equitable right to acquire the home.

Based on the current market uncertainties, you are wise to explore various strategies for maximizing your profit from your recent home flip. I suspect we will be seeing more rent-to-own transactions in the foreseeable future.

Harvey S. Jacobs is a real estate lawyer with Jacobs & Associates Attorneys at Law in Rockville. He is an active real estate attorney, investor, landlord, lender and settlement attorney. This column is not legal advice and should not be acted upon without obtaining your own legal counsel. Contact him at jacobs@jacobs-associates.com, jacobs-associates.com or ask@thehouselawyer.com, or call 301-417-4144.

ould the coronavirus pandemic stop a home sale? Read your contract closely to see if there’s a key clause. (iStock)

Published on April 14, 2020 at 9:00 a.m. EDT

The unprecedented coronavirus pandemic is having a major impact on real estate transactions. Parties under contract to buy or sell their homes are concerned about their contract’s viability and their legal rights under that contract.

In law, there is a doctrine called “force majeure” that excuses or permits a party to delay its performance under an otherwise legally enforceable contract when certain events occur. Force majeure means “greater force.” A force majeure event is derived from the French Napoleonic Code. Force majeure events are often defined in contracts to include political events such as wars, insurrections, riots, strikes, lockouts, terrorist threats or actions, or explosions. A force majeure event is often referred to as an act of God or act of nature, such as hurricanes, floods, earthquakes, landslides, tornadoes, tsunamis, volcanic eruptions, sinkholes and storms.

Generally, losing one’s job, asset diminution, financial reverses or general uncertainty about the future are not force majeure events, though they may be relevant factors that lenders will consider when approving or denying a buyer’s loan application.

Courts look to the specific force majeure clause language in a contract to determine whether a certain event is covered. Absent a force majeure clause, the courts will generally enforce the contract terms as written.

The current Greater Capital Area Association of Realtors sales contract does not contain a force majeure clause. The association has recently issued a coronavirus addendum. The addendum allows a buyer and seller to agree in advance to extend deadlines if certain events occur. Those coronavirus-related events are called permitted delays. Permitted delays include the buyer or seller being exposed to or infected with the coronavirus or diagnosed with covid-19, the buyer or seller being quarantined or not permitted to travel, the buyer’s settlement attorney or lender being unable to complete the transaction, and other similar causes related to the coronavirus outbreak that are beyond a buyer’s or seller’s reasonable control.

Events that may be beyond a buyer’s or seller’s reasonable control may be scheduling home, pest, radon or other contractually required inspections. Sellers may be understandably reluctant to allow home access for showings and/or walk-throughs immediately before settlement. If they do allow access, many sellers are requiring visitors to wear gloves, masks, shoe coverings and perhaps even submitting to have their temperature taken. Home inspectors are reluctant to make their inspections. Lenders report that they are having difficulty getting appraisals done in a timely manner and in verifying buyers’ employment immediately before settlement since so many employers’ businesses are closed. Open houses have become risky and, where legal, severely limited, but virtual open houses may still be held via the Internet and may become the wave of the future.

All stakeholders in the residential real estate industry are collaborating to continue to allow settlements to proceed while complying with the public necessity to stay home. Emergency declarations and stay-at-home orders issued by governors and mayors around the country have defined lenders and settlement attorneys as “essential businesses” so that parties ready to go to settlement may do so. These governmental acts have also, in many states, authorized electronic signatures and remote online notarization to be used so that settlements can occur without having to engage in face-to-face settlements. Emergency orders have authorized and directed county recording officials to accept electronic signatures via electronic recordings. Lenders are expediting approvals for using digital promissory notes and permitting settlement attorneys to conduct online settlements and remote online notarizations. Settlement companies are rushing to implement the available technology for virtual settlements. But these coordinated steps will take time to fully integrate. In the meantime, curbside settlements, settlements held in strictly controlled and disinfected rooms, and other improvised measures will be the norm to permit buyers and sellers to complete what is typically the most important transaction of their lives.

Harvey S. Jacobs is a real estate lawyer with Jacobs & Associates Attorneys at Law in Rockville. He is an active real estate attorney, investor, landlord, lender and settlement attorney. This column is not legal advice and should not be acted upon without obtaining your own legal counsel. Contact him at jacobs@jacobs-associates.com, jacobs-associates.com or ask@thehouselawyer.com, or call 301-417-4144.

A 1031 exchange allows you to defer liability for all federal capital gains and depreciation recapture taxes. (iStock)

Published in the Washington Post March 9, 2020 at 9:00 a.m. EDT

Q: I am selling a house in the District of Columbia that I bought 10 years ago, renovated and have rented out as an investment ever since. I paid $400,000 and can now sell for $800,000. I immediately renovated the kitchen and baths, which cost $100,000. At settlement, I plan on paying $48,000 in real estate commissions, $11,600 in D.C. transfer tax and an additional $10,400 in closing costs and seller credits to buyer. My pretax cash profit should be about $330,000. What are the tax implications, and what can I do to maximize my after-tax profits? — Savvy Seller

A: Congratulations on successfully investing in a rental property. When you sell your rental property, you will incur federal and state long-term capital gains and depreciation recapture taxes. You may also incur the Net Investment Income Tax, which imposes an additional 3.8 percent tax on your net investment income above certain thresholds.

Capital gain is the difference between your selling price and your adjusted tax basis. The Internal Revenue Service classifies capital gains as either short or long term. Gain on the property sales held for one year or less is considered short term and is taxed at your ordinary income tax rate. Gain on property sales held for more than one year is classified as a long-term capital gain and is taxed at rates ranging from 0 percent to 20 percent. Most homeowners will pay at the 15 percent rate.

Although you state that your pretax cash profit is $330,000, your taxable long-term capital gain is only $230,000. Taxable capital gain is calculated by taking your sales price ($800,000), minus commissions and closing costs ($70,000), minus your adjusted tax basis ($500,000). Your adjusted tax basis is your original cost plus your capital improvements. “Assuming you are in the 15 percent capital gains tax bracket, your federal capital gains tax liability would be $34,500,” said Eric J. Wexler, a Rockville, Md., tax attorney and CPA.

IRS regulations generally require that you depreciate residential rental property over 27.5 years (3.636 percent per year). Because land does not wear out, the IRS does not permit you to depreciate the purchase price attributable to the land. To calculate your depreciation deductions, we assume: your $400,000 purchase price was allocated equally between the land and the original improvements; and that the additional capital improvements were made before the home was placed into service as a rental property. As such, your property’s “depreciable base” is $300,000. Accordingly, you were able to take $10,908 annually for the 10 years it was rented, for $109,080 in total cumulative depreciation.

“This non-cash tax deduction may have reduced your annual taxes,” Wexler said. “But now that you are selling, this non-cash tax deduction must be paid back, in part, as depreciation recapture tax. So, in addition to your $34,500 in capital gains tax, you will incur $27,270 in federal depreciation recapture tax, for $61,770 in total federal tax liability.” Your pretax cash profit minus your federal tax liability results in $268,230 in after-tax profits, which will be further reduced by state capital gains and depreciation recapture taxes. “Any taxable gain may be offset by any suspended losses that you were not able to use during the life of the property,” Wexler said.

Because this is investment-only property, you are not eligible to use the $250,000 ($500,000 for a married couple) capital gains exclusion available when you sell your primary residence. IRS Pub. 544, available online at irs.gov, contains detailed instructions for calculating capital gains and depreciation recapture for residential rental property.

Because your current plan to sell investment property results in significant tax liabilities with no real tax advantages, one way to dramatically increase your after-tax profit is to consider using a 1031 exchange. This IRS code section allows you to exchange your D.C. property and reinvest your cash in another like-kind replacement investment, such as other rental real estate or a Delaware Statutory Trust.

A 1031 exchange requires you to identify your replacement property within 45 days and to close on your replacement property within 180 days of settling your D.C. property. A 1031 exchange allows you to defer liability for all federal capital gains and depreciation recapture taxes. You can sell your D.C. property and pay no federal income taxes on that gain so long as you use a qualified exchange intermediary to hold your funds and you reinvest your entire sales proceeds in a new investment property having a value equal to or greater than your D.C. property.

Harvey S. Jacobs is a real estate lawyer with Jacobs & Associates Attorneys At Law in Washington and Rockville, Md. He is an active real estate investor, landlord, settlement attorney, lender and associate real estate broker. This column is not legal advice and should not be acted upon without obtaining your own legal counsel. Contact Jacobs at 301-417-4144, Jacobs@Jacobs-Associates.com or Ask@thehouselawyer.com.

Scammers send massive numbers of malware-embedded emails containing real estate settlement subject lines such as: “URGENT There is a problem with your settlement.” Innocent home buyers fear something may have gone awry with their settlement and open and/or click on the infected email. (iStock)

Published Jan. 6, 2020 at 9:00 a.m. EST

As if buying, selling or refinancing your home were not stressful enough, consumers must now be aware of an increasingly insidious form of email-based real estate fraud. The FBI categorizes this crime as Business Email Compromise (BEC). In 2018, it is estimated that 11,300 consumers lost $150 million to BEC crimes.

BEC crimes begin when scammers induce email recipients to open or click on a link in an infected email.

When the recipient inadvertently opens or clicks on the fake email, a malware program is installed on the recipient’s computer. Once that malware embeds itself, it allows the scammer to monitor the recipient’s emails for words like “settlement date,” “wire instructions” or “cashier’s checks.”

At just the appropriate time, the scammer, impersonating the title company, will send out a fake email instructing the victim to wire funds to a bank account that turns out to be the scammer’s own account. Thinking it has received official title company wire instructions, the victim willingly wires their funds.

There are numerous techniques scammers use to get real estate settlement parties to click on fake emails.

One technique is to spoof the legitimate sender’s email address. Scammers send fake emails from accounts that are nearly identical to the legitimate sender’s email addresses. For example, law firm email addresses that contain the word “law” are spoofed when scammers change the word law to lavv. On a mobile device, distinguishing a “w” from a “vv” can be almost impossible.

Another technique uses social engineering by appealing to the recipient’s sense of urgency, fear or curiosity.

Scammers send massive numbers of malware-embedded emails containing real estate settlement subject lines such as: “URGENT There is a problem with your settlement.” Innocent home buyers fear something may have gone awry with their settlement and open and/or click on the infected email.

From that point forward, the scammer can access all transaction details. These emails are referred to as “phishing” emails since they are designed to hook their recipients into clicking on a link in those emails or even just opening them.

Increasingly, scammers are targeting specific recipients by taking advantage of all the publicly available information about a real estate transaction. They “phish” the listing agent, and if successful, they gain access to that agent’s email.

With that access, the scammer obtains information such as the names and email addresses for buyer, seller settlement company and lender as well as the loan amount and the proposed settlement date.

Armed with this data, scammers pose as the settlement company and email the buyer well before the settlement date and falsely instruct them to wire their “cash to close” immediately. Unwitting buyers comply. It is only later, when the real settlement company contacts the buyer, that the horrible truth is discovered. By then, it is too late for law enforcement to trace the funds or catch the scammers.

“Scammers send us phishing emails every day, and sometimes numerous times in a day,” said John Cotter, president and CEO of Passport Title Services in Rockville, Md. “It is imperative that before consumers wire settlement funds, they scrutinize the sender’s email address. We no longer accept wiring instructions via email unless verified by a phone call.”

With this much at risk, the real estate industry has embarked on a public education campaign to raise awareness of these crimes. The American Land Title Association (ALTA) launched the Coalition to Stop Real Estate Wire Fraud with consumer resources at www.StopWireFraud.org.

If you do become a victim of BEC crime, “immediately call your bank and ask them to issue a recall notice for your wire, report the crime to BEC.IC3.gov and call your regional FBI office and police department,” said Justin B. Ailes, senior vice president of policy at ALTA. “When these steps are followed within 24 hours of the wire transfer, the FBI’s Internet Crime Complaint Center’s Recovery Asset Team has recovered 75 percent of compromised funds.”

To avoid being victimized, the public should carefully examine the sender’s email address to confirm it is coming from a legitimate sender. If in doubt, do not reply; rather, forward the email back to the known email address.

Do not use phrases like “wire instructions” in the subject line of your emails. Call and confirm all wire transfer instructions by phone using a previously known phone number or by accessing the title company’s website.

Do not call the phone number in the suspicious email. Minimize the number of people who get copied on real estate settlement-related transactions by sending transaction details only to those on a need-to-know basis.

Start a new email thread each time you email anyone involved in the transaction, especially when communicating about the financial part of the transaction.

Harvey S. Jacobs is a real estate lawyer with Jacobs & Associates in Washington. He is an active real estate investor, landlord, settlement attorney and lender. This column is not legal advice and should not be acted upon without obtaining your own legal counsel. Submit your questions to: Ask@theHouseLawyer.Com, or call Harvey at 301-417-4144.